The global High-Density Polyethylene (HDPE) market has entered a period of sharp corrective pricing. The second quarter of 2026 has witnessed an unwinding of the intense geopolitical risk premiums that dictated polyolefin pricing during the opening months of the year.

Following a period where escalating conflicts and supply-chain anxieties sent shocks through the global energy and petrochemical sectors, the market throughout May and early June has swiftly pivoted.

For both the US and Europe, HDPE Injection Molding grades are undergoing a necessary consolidation as macroeconomic realities overwrite previous supply panics.

From Geopolitical Spikes to Secondary Consolidation

The macroeconomic landscape of early 2026 was largely defined by severe energy market disruptions. Following the sudden escalation of the West Asia crisis starting in late February, global energy corridors faced unprecedented volatility.

Global Brent crude surged toward the $100 per barrel mark, forcing international petrochemical feedstocks and monomer contracts upward in a classic cost-push inflationary spiral.

During that initial phase, frantic panic-buying from downstream converters desperate to secure inventory against potential shipping blocks artificially drove polyolefin prices to historic highs.

However, as spring progressed into June, the initial shock waves faded. Although regional tensions remain an ongoing element of macroeconomic uncertainty, the logistics bottlenecks and catastrophic supply stoppages feared by the market failed to fully materialize.

Consequently, global crude oil benchmarks began to cool, and the heavy premium baked into the price of ethylene derivatives rapidly deflated. This shift cleared the way for a sharp downward correction in resin prices as the market adjusted to actual downstream consumption patterns.

Weekly Price Shifts: Tracking the Transatlantic Deflation

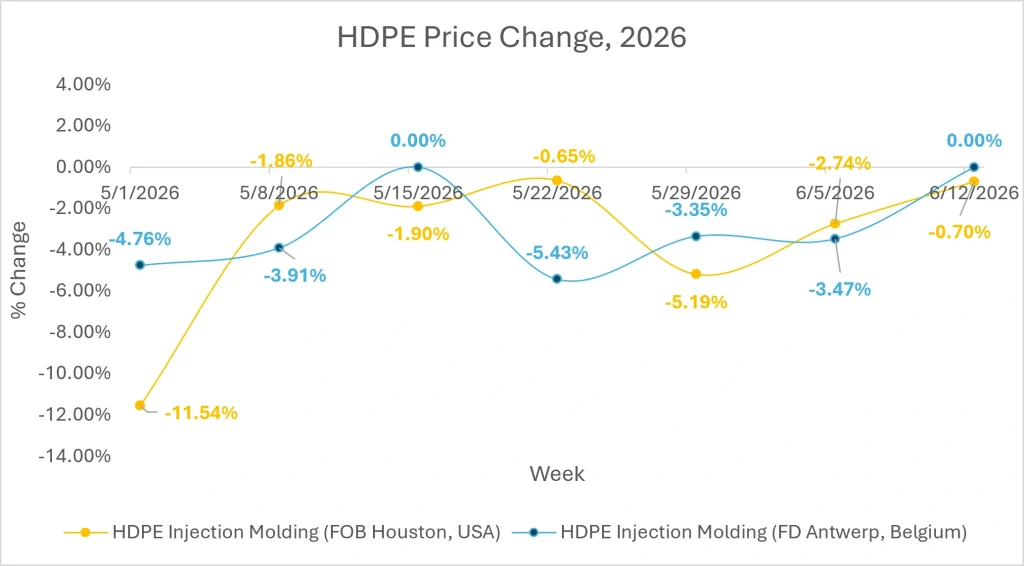

The pricing data below illustrates how the deflating energy premium hit the primary export and regional hubs FOB Houston (USA) and FD Antwerp (Belgium) for HDPE Injection Molding Grade:

US Gulf Coast: FOB Houston Absorbs the Shock

The domestic US petrochemical sector felt the immediate impact of the cooling global market at the turn of May. A massive -11.54% price drop in the first week of May marked a structural reset.

- The Margin Realignment: As upstream oil and gas feedstocks shed their conflict-driven premiums, integrated US producers on the Gulf Coast lost the leverage required to sustain historic-high resin quotes. Export arbitrage windows narrowed as global buyers recognized the shifting tide.

- Late-May Volatility: After a temporary pause mid-month, a secondary price correction hit the Houston hub during the week ending May 29, triggering a further -5.19% drop. This was primarily driven by international buyers stepping back from spot purchases, waiting for the pricing floor to establish itself.

- June Stabilization: By mid-June, the intense downward momentum successfully exhausted itself. The marginal -0.70% adjustment on June 12 indicates that US export pricing has finally bottomed out, moving closer to production cost baselines.

Source: Price Watch™ HDPE Prices

European Hubs: FD Antwerp Reacts to Softening Upstream Costs

Europe’s polymer sector has followed a remarkably similar trajectory, though its adjustments were staggered due to regional monomer contract timings. The region entered May with consecutive drops of -4.76% and -3.91% as the immediate panic over Mediterranean and West Asian transport routes normalized into steady, predictable flows.

The pricing peaks of the first quarter built an unsustainable foundation. Once the initial raw material supply fears eased, European converters immediately pulled back on ordering, executing a hand-to-mouth procurement strategy.

- The Mid-May Cliff: While Europe saw a temporary plateau on May 15, the market experienced its steepest correction during the week of May 22, diving -5.43%. This slide reflected a combination of cheaper import alternatives filtering into Northern Europe and falling domestic naphtha values.

- Finding the Floor: In line with the trends observed in the US, the European market achieved a much-needed baseline by June 12, registering a flat 0.00% change. With margins severely compressed, European petrochemical complexes responded by proactively managing operating rates, effectively capping the multi-week downward cycle.

Dynamic Market Catalysts

The Raw Material Cooldown

The primary catalyst behind this multi-week price slide is the rapid decompression of the upstream cost structure. The direct relationship between volatile crude benchmarks and polymer pricing was highly evident: as West Asian logistics panics subsided, the immediate collapse of oil-driven premiums translated directly into lower production costs for downstream polyolefins.

The Stance of Downstream Convertors

Rather than chasing the market downward, industrial molders and consumer rigid packaging converters in both regions chose to step aside.

Having heavily stocked up on expensive material during the Q1 crisis, processing plants spent much of May and June burning through existing stockpiles, refusing to place major bulk orders until raw material costs stabilized.

Forward Looking Perspective

As the market advances through June, the frantic price drops that characterized May have clearly decelerated. The flat performance in Europe and the near stabilization in Houston during the second week of June signify that the worst of the post-panic price unwinding is complete.

Moving deeper into summer, market participants can expect a highly conservative trading environment. Lacking a major renewed spike in energy markets or a sudden surge in underlying infrastructure demand, transatlantic HDPE prices are positioned to trade sideways within a narrow, stable band.

Follow Price Watch™ on LinkedIn for real-time raw material insights, pricing trends, supply chain intelligence, and market updates shaping global commodity markets.