The Inflation Nobody Sees

Every morning, millions of Indian households begin their day with a pouch of milk. From May 14, Amul increased prices by ₹2 per litre nationwide, citing higher input costs. Yet the real driver is invisible: petroleum-derived plastic granules called polymers.

From milk pouches and biscuit wrappers to edible oil containers and paper cups, these tiny beads silently determine what consumers pay. As crude oil markets grow volatile, polymers have become a material inflation cascade, one raw material category triggering price increases across seemingly unrelated industries simultaneously.

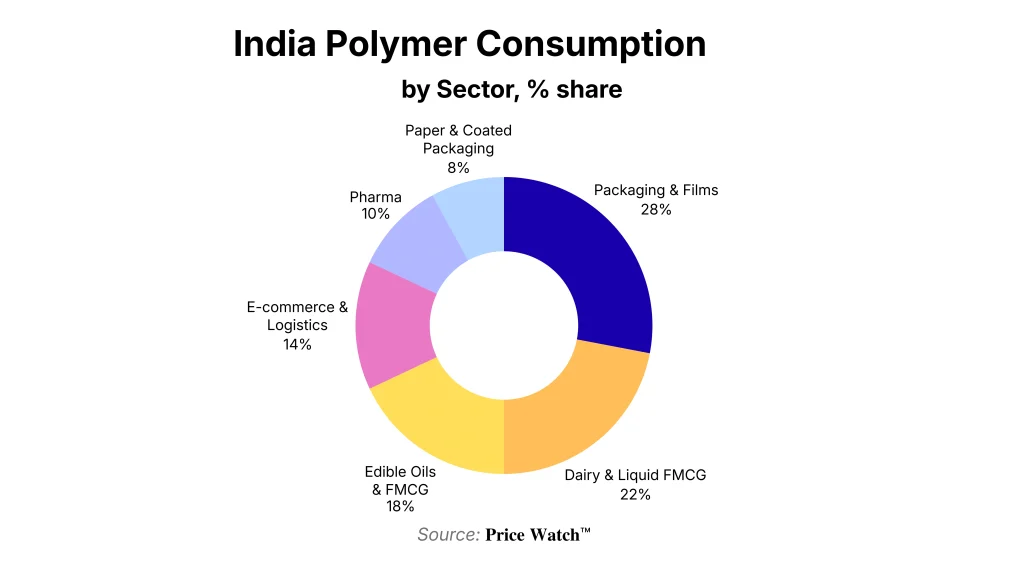

Figure 1: Indian Polymer Consumption by Sector (%)

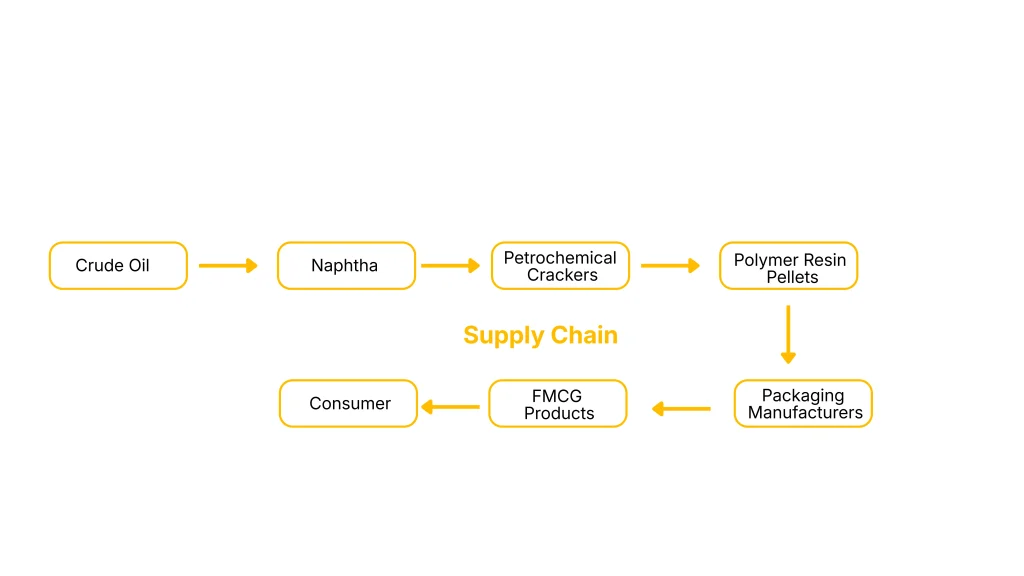

India’s Polymer Economy: The Hidden Foundation of Consumer Goods

Polymers such as:

- Polyethylene (PE)

- Polypropylene (PP)

- Polyethylene Terephthalate (PET)

- High-Density Polyethylene (HDPE)

- Low-Density Polyethylene (LDPE)

are produced from crude oil and natural gas derivatives through energy-intensive petrochemical processes.

The supply chain is remarkably interconnected:

A rise in crude oil prices does not merely affect fuel stations, it directly raises the cost of polymer resin production, which then propagates through the entire manufacturing ecosystem.

The Global Forces Behind Rising Polymer Prices

-

Crude Oil Volatility

Polymers remain fundamentally linked to petroleum markets.

Recent years have witnessed:

- Geopolitical conflicts affecting energy routes

- OPEC production adjustments

- Refinery maintenance disruptions

- Sanctions on major oil-exporting nations

Each disturbance affects naphtha pricing, which subsequently influences polymer production costs.

-

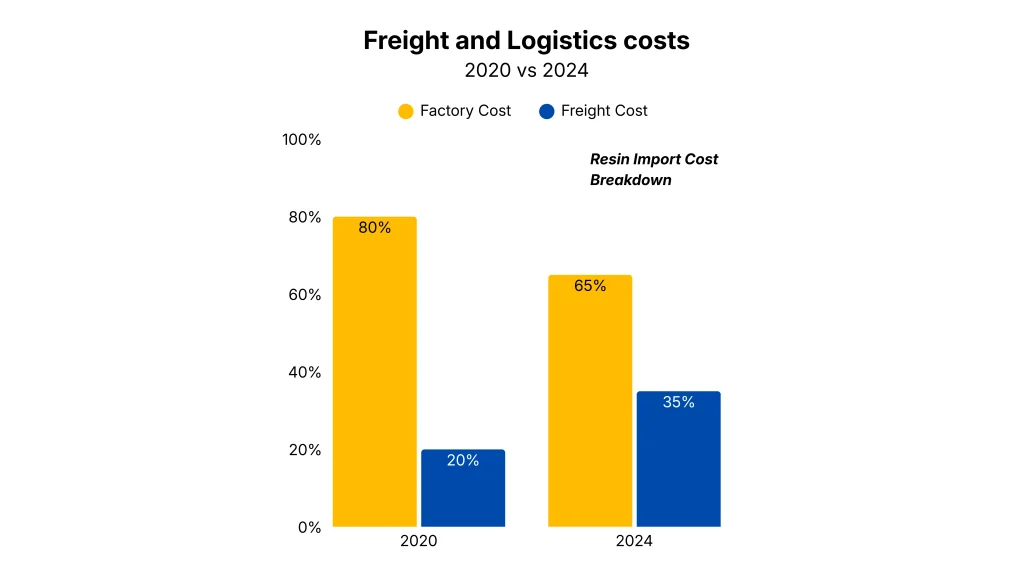

The Freight Cost Shock

Following pandemic-era disruptions and later Red Sea shipping disturbances, freight rates experienced unprecedented fluctuations.

For resin importers, transportation costs became a major pricing component.

| Year | Factory Cost | Freight Cost |

| 2020 | 80% | 20% |

| 2024 | 65% | 35% |

In some cases, logistics costs rose faster than raw material costs themselves.

-

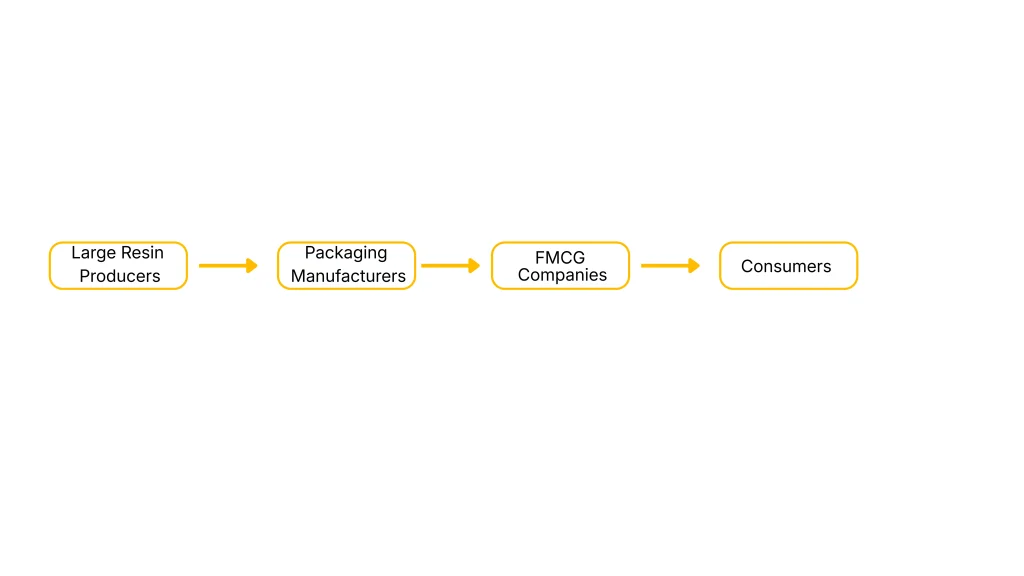

Market Concentration

India’s polymer market remains highly consolidated.

Large integrated petrochemical producers possess substantial pricing power, while thousands of downstream converters operate on thin margins.

This creates a structural imbalance:

Every pricing revision at the top reverberates throughout the supply chain.

The Global Forces Behind Rising Polymer Prices

In 2026, a cascade of geopolitical shocks dismantled global polymer supply chains:

- QatarEnergy Force Majeure: Missile strikes disrupted nearly 20% of global LNG export capacity. The destruction of Ras Laffan removed 12.8 million MT of annual liquefaction capacity, spiking European ethylene costs.

- Strait of Hormuz Blockade: Near-closure disrupted ~25% of global polyethylene exports, forcing Indian buyers to compete for scarce alternatives at premium prices.

- Sadara Complex Shutdown: The suspension of Saudi Arabia’s Sadara facility removed 1.1 million MT of polyethylene capacity, creating a global supply vacuum.

- India-Specific Pressures: INR depreciation made imports costlier. Government LPG restrictions tightened feedstock availability. Packaging converters revised multi-layer film fees 8–10 times within a single quarter.

Figure 2: Rising Freight Share in Resin Import Cost (2020 vs 2024)

The Milk Pouch, Shrinkflation, and the FMCG Crisis

A milk pouch is not simple plastic, it is an engineered multilayer film (LDPE outer layer, LLDPE structural layer, food-grade inner layer) requiring premium virgin resin. No cheaper substitute meets Amul’s food-safety and high-speed filling requirements.

Every fraction-of-a-paisa rise per pouch, across millions of units daily, becomes impossible for cooperatives to absorb, resulting in the ₹2/litre hike passed to consumers.

Biscuit brands responded differently: keeping the ₹5 price point while shrinking pack weights from 64 g to 55 g. Edible oil producers face a double squeeze, higher commodity costs upstream and surging HDPE bottle costs downstream.

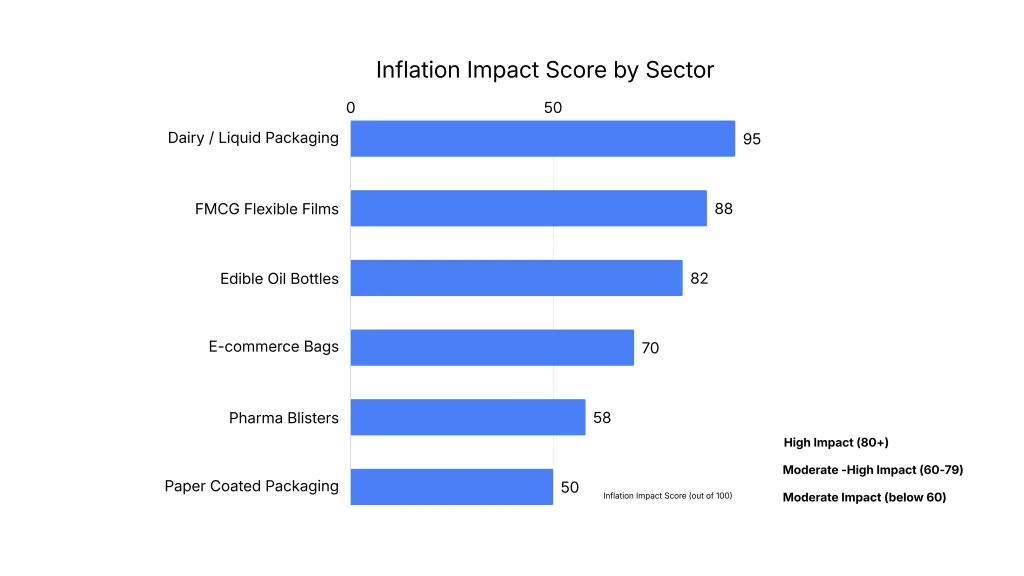

Figure 3: Polymer Inflation Impact Score by Sector India 2026

The Great Migration to Paper and Its Irony

As polymer costs soared, brands rushed to paper alternatives. Paper demand exploded, pulp prices surged, and paper mills faced the same inflationary crisis. The deeper irony: most ‘paper’ products, coffee cups, juice cartons, frozen food packaging, still require thin PE barrier coatings.

Companies that fled polymer inflation simply imported it through the back door, creating a triple inflation loop: oil shocks → polymer inflation → paper substitution → pulp inflation → polymer-coated paper demand → additional polymer demand. Each cycle reinforces the next.

The Invisible Inflation Engine

A missile strike in Qatar, a factory shutdown in Jubail, a currency shift in Delhi, these events, invisible to most consumers, raised the cost of milk, shrank biscuit packs, and disrupted paper mills across India.

Until mechanical recycling scales, bio-based coatings mature, and feedstock sources diversify, polymer prices will continue shaping Indian household budgets in ways most consumers never see, yet feel every single day.

Key Takeaway

The next time a milk pouch costs more, a biscuit feels lighter, or a takeaway cup is priced higher, look past the product. The answer lies in a handful of petroleum-derived pellets produced thousands of kilometres away, silently driving the economics of everyday Indian life.

Follow Price Watch™ on LinkedIn for real-time raw material insights, pricing trends, supply chain intelligence, and market updates shaping global commodity markets.