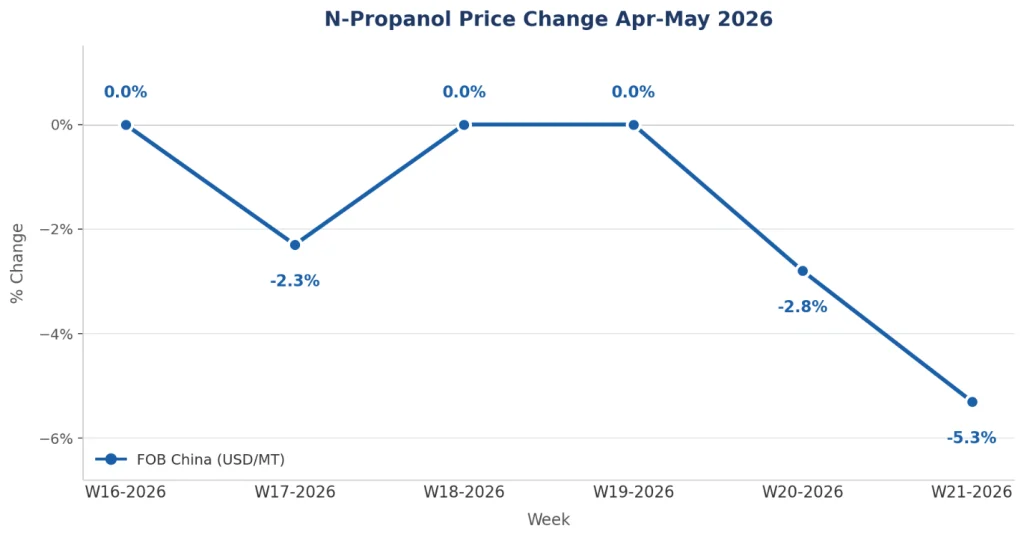

China’s FOB price for N-propanol has dropped close to 10% since W16 2026. That is not just a correction. It signals a real shift in the supply balance that buyers across Asia and Latin America are watching carefully.

The key driver is propylene, the primary feedstock for N-propanol. Crude oil prices have decreased over the past month, and with them, propylene contract prices in Asia have eased. Chinese producers, already running at high utilization rates, are now under pressure to move inventory before margins compress further.

Source: Price Watch™ N-Propanol Prices

Supply Chain Disruption and Strait of Hormuz: N-Propanol Import Risk

Freight routes through the Strait of Hormuz remain a concern for importers in India and Southeast Asia. Shipping costs on Middle East routes have stayed elevated, though they have not escalated sharply in recent weeks. Any renewed tension in the region would push CIF prices higher, even if FOB values stay flat.

During the Iran-Israel conflict earlier in the reporting period, N-propanol import prices across key Asian markets rose by approximately 37%, driven by a spike in freight premiums and precautionary buying. That spike has since partially reversed, but the risk has not disappeared.

Value Chain Impact: Solvents, Pharmaceuticals and Coatings

N-propanol is widely used across pharma, coatings, and cleaning product sectors. Falling import prices in India give formulators a short window to restock at lower cost. The Ex-Kandla domestic price has also come off, though it still carries a significant premium over import parity.

Argentina saw a brief uptick in W19 2026, likely tied to limited vessel availability on the South America route combined with a temporary demand push from the local pharma sector. That reversed sharply in W20 and W21 as Chinese export volumes picked up.

Short-Term Outlook for N-Propanol: 1 to 3 Months

Prices are likely to stay soft through June and into July 2026, unless crude oil recovers sharply or freight routes face a fresh disruption. Propylene supply in China is adequate, and new capacity additions in the first half of 2026 have added downward pressure on feedstock costs.

- India domestic prices at Ex-Kandla are sticky. The gap with CIF import levels may narrow as buyers consider switching to imports over the next four to eight weeks.

- A re-escalation in the Middle East or any disruption near the Strait of Hormuz could reverse this trend quickly. Freight insurance premiums are already above historical norms on affected routes.

If Chinese producers start cutting run rates to defend prices, will the FOB floor hold, or is there further room to fall before the next demand cycle kicks in?

Follow Price Watch™ on LinkedIn for real-time raw material insights, pricing trends, supply chain intelligence, and market updates shaping global commodity markets.