The global acetic acid market is on a steady growth path, supported by broad-based demand from polymers, textiles, packaging, construction chemicals, solvents, and food processing. Worldwide demand is estimated at about 16,317 KT, with Asia-Pacific remaining the leading consumption center. This demand profile is closely tied to the scale of downstream industries such as purified terephthalic acid (PTA), vinyl acetate monomer (VAM), acetate esters, and acetic anhydride, all of which continue to shape the market’s structure and growth direction.

Asia-Pacific Dominates Global Consumption

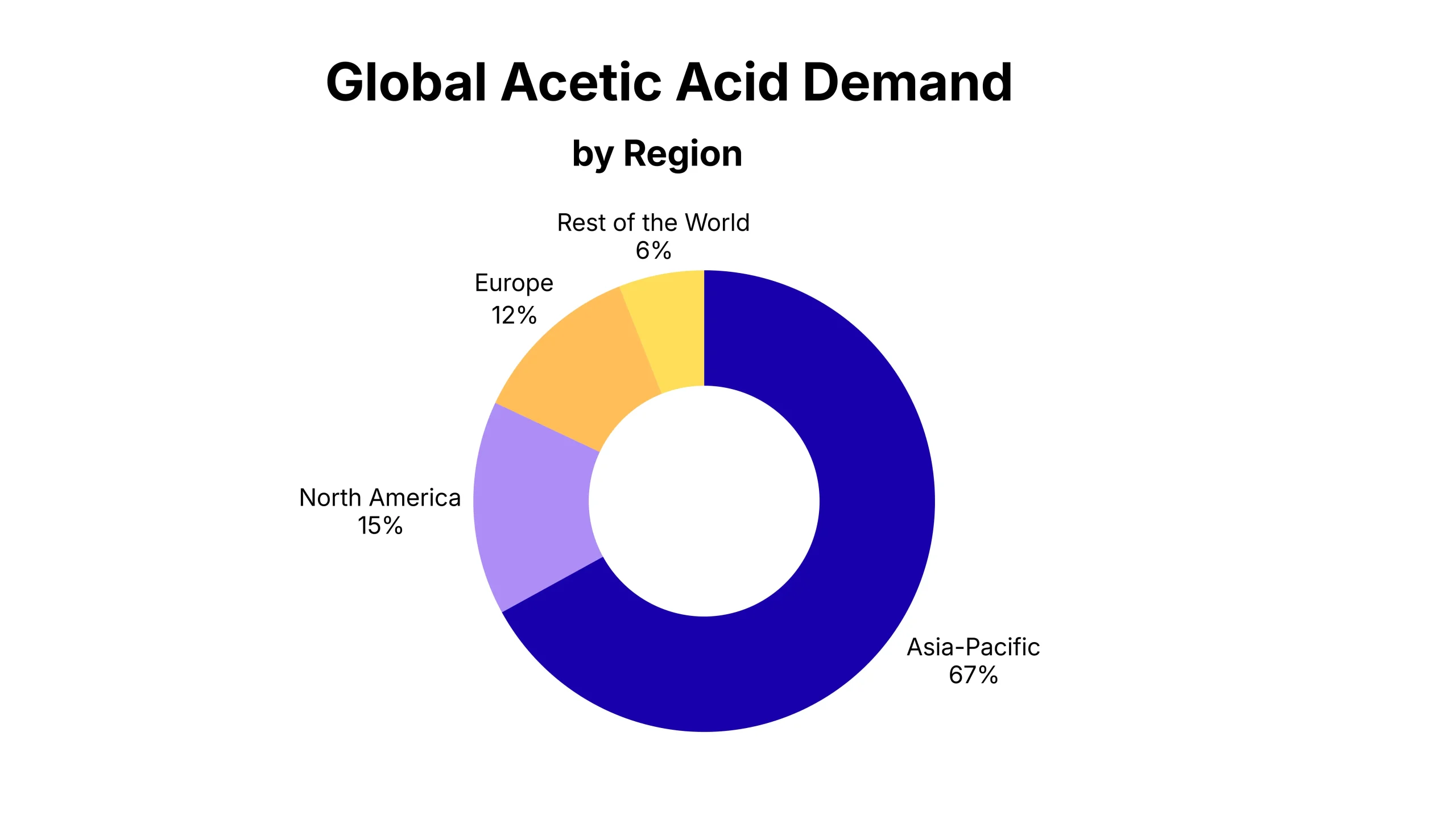

Regional demand remains heavily concentrated in Asia-Pacific, which accounts for nearly 67% of global acetic acid consumption. China alone represents around 46% of worldwide demand, making it by far the largest individual market. North America contributes roughly 15%, while Europe holds close to 12%, with the balance spread across Latin America, the Middle East, and Africa. Asia’s dominance reflects the region’s extensive manufacturing base, integrated petrochemical networks, strong export orientation, and continued expansion in polymer and textile production.

Within Asia-Pacific, demand is further concentrated in a number of major industrial clusters. In China, provinces such as Jiangsu, Shandong, Zhejiang, and Fujian are among the most important acetyl-chain manufacturing centers. In India, Gujarat and Maharashtra are emerging as major demand hubs due to rising investment in chemicals, packaging, adhesives, textiles, and pharmaceuticals. Together, these industrial belts account for more than 40% of global acetic acid demand, highlighting the importance of integrated production ecosystems and export-linked manufacturing growth.

Source: Price-Watch™ Data

PTA and VAM Demand Continues to Drive Structural Growth

A key engine of acetic acid demand is the continued growth of the PTA sector. PTA serves as an essential feedstock for polyester fiber and polyethylene terephthalate (PET) resin, both of which are widely used in textiles, bottles, industrial yarns, and packaging materials. As consumption of polyester-based products and PET packaging rises, demand for PTA has increased accordingly, creating a direct uplift for acetic acid. This trend is especially visible in Asia-Pacific, where China and India continue to expand their textile and packaging industries. Demand is also being reinforced by the preference for lightweight, durable, and recyclable packaging solutions.

VAM is another major outlet for acetic acid consumption. It is widely used in the production of adhesives, paints, coatings, construction chemicals, paper processing materials, solar encapsulants, and packaging products. Rising urbanization and infrastructure spending in developing markets have supported higher demand for these end uses, thereby strengthening VAM production. In addition, the increasing use of EVA-based materials in solar panels and selected automotive applications is further supporting growth across the broader acetyl value chain.

China’s Integrated Chemical Ecosystem Keeps It Ahead

China’s leading position in the global acetic acid market is supported by a strong combination of feedstock access, scale, and downstream integration. The country benefits from substantial coal-to-methanol and methanol carbonylation capacity, which helps maintain raw material availability and cost competitiveness. It also hosts large integrated chemical complexes where acetic acid, PTA, and VAM facilities are often located close to one another, improving logistics and operating efficiency. These advantages are reinforced by strong domestic demand from the textile, packaging, automotive, and electronics sectors, as well as policy support aimed at strengthening local manufacturing and chemical self-sufficiency.

India Emerges as the Next Strategic Growth Market

India is becoming an increasingly important growth market for acetic acid. Expanding manufacturing activity, stronger pharmaceutical output, rising packaged food consumption, and ongoing infrastructure development are all contributing to higher demand. Gujarat and Maharashtra continue to stand out as major chemical manufacturing centers because of their port connectivity, refinery integration, and industrial investment base. As companies diversify supply chains and look beyond traditional production centers, India is gaining attention as a strategic alternative for future acetyl demand growth.

Beyond regional growth patterns, the market is also being shaped by a broader shift toward supply chain integration and localization. Producers are increasingly investing in downstream integration to improve operating efficiency, reduce transportation exposure, and strengthen supply reliability. This strategy has gained importance in the wake of geopolitical disruptions and logistics bottlenecks, which highlighted the risks associated with highly dispersed global chemical supply chains.

Sustainability Pressures Begin to Influence Production Strategy

Sustainability is also emerging as an important consideration in the acetic acid industry. While production remains largely dependent on methanol-based routes, interest in bio-based and lower-carbon alternatives is gradually increasing. Regulatory pressure related to emissions, especially in Europe and parts of Asia, is encouraging producers to assess cleaner technologies and more energy-efficient processes. Even so, widespread commercial adoption remains limited, as producers continue to weigh environmental benefits against cost competitiveness and technical feasibility.

Despite favorable long-term fundamentals, the market continues to face several challenges. One of the most important is feedstock price volatility. Methanol, the main raw material used in acetic acid production, is influenced by movements in natural gas, coal, and crude oil markets. As a result, sharp swings in energy prices can quickly affect production costs, margins, and pricing stability for acetic acid producers.

Geopolitical uncertainty and supply chain disruption remain additional risk factors. Trade disputes, freight constraints, regional conflicts, and export controls can interfere with raw material availability and alter trade flows. These issues are particularly significant in the chemical sector, where production and demand are often concentrated in a limited number of interconnected regions.

Overcapacity in China is another issue closely watched by market participants. Rapid capacity additions can create short-term imbalances between supply and demand, putting pressure on global prices and producer profitability. At the same time, stricter environmental enforcement in China can lead to temporary shutdowns or lower operating rates, which may introduce periodic supply volatility into the global market.

The cyclical nature of downstream sectors also affects market stability. Industries such as textiles, construction, automotive, and packaging are sensitive to economic conditions, consumer demand, and industrial output trends. During periods of slower growth or weaker spending, demand for PTA, VAM, and solvent derivatives can soften, which in turn reduces acetic acid consumption. This keeps the market closely linked to broader manufacturing and business cycles.

Acetic Acid is Becoming a Strategic Industrial Molecule

Looking ahead, the global acetic acid market is expected to sustain steady long-term growth, supported by industrialization, urban expansion, and rising demand for polymers across emerging economies. Asia-Pacific is likely to remain the core demand center, with China and India continuing to account for much of the incremental growth. The further development of manufacturing clusters in regions such as Jiangsu, Shandong, Zhejiang, Fujian, Gujarat, and Maharashtra is expected to deepen regional integration and strengthen Asia’s role in the global acetyl market.

In summary, the global acetic acid market is evolving into a more integrated, Asia-focused, and downstream-led industry. Producers with strong feedstock positions, diversified end-use exposure, and efficient supply chain capabilities are likely to be best placed to benefit from future growth while managing the risks associated with volatility and market concentration.

At Price-Watch™, we provide real-time acetic acid pricing intelligence, feedstock monitoring, freight tracking, plant operating assessments, and regional trade flow analysis across key global markets. From methanol cost movements and Chinese operating rate changes to CIF arbitrage spreads and downstream PTA and VAM demand trends, our intelligence platform helps procurement teams, traders, and manufacturers react faster, reduce exposure, and identify market shifts before they impact profitability.

Follow Price Watch™ on LinkedIn for real-time raw material insights, pricing trends, supply chain intelligence, and market updates shaping global commodity markets.